The New Observability Intents of 2026 — and How to Position for Them

A field note for observability marketing leaders on where buyer intent has moved, and why the vendors reading it at the account level are winning the shortlist.

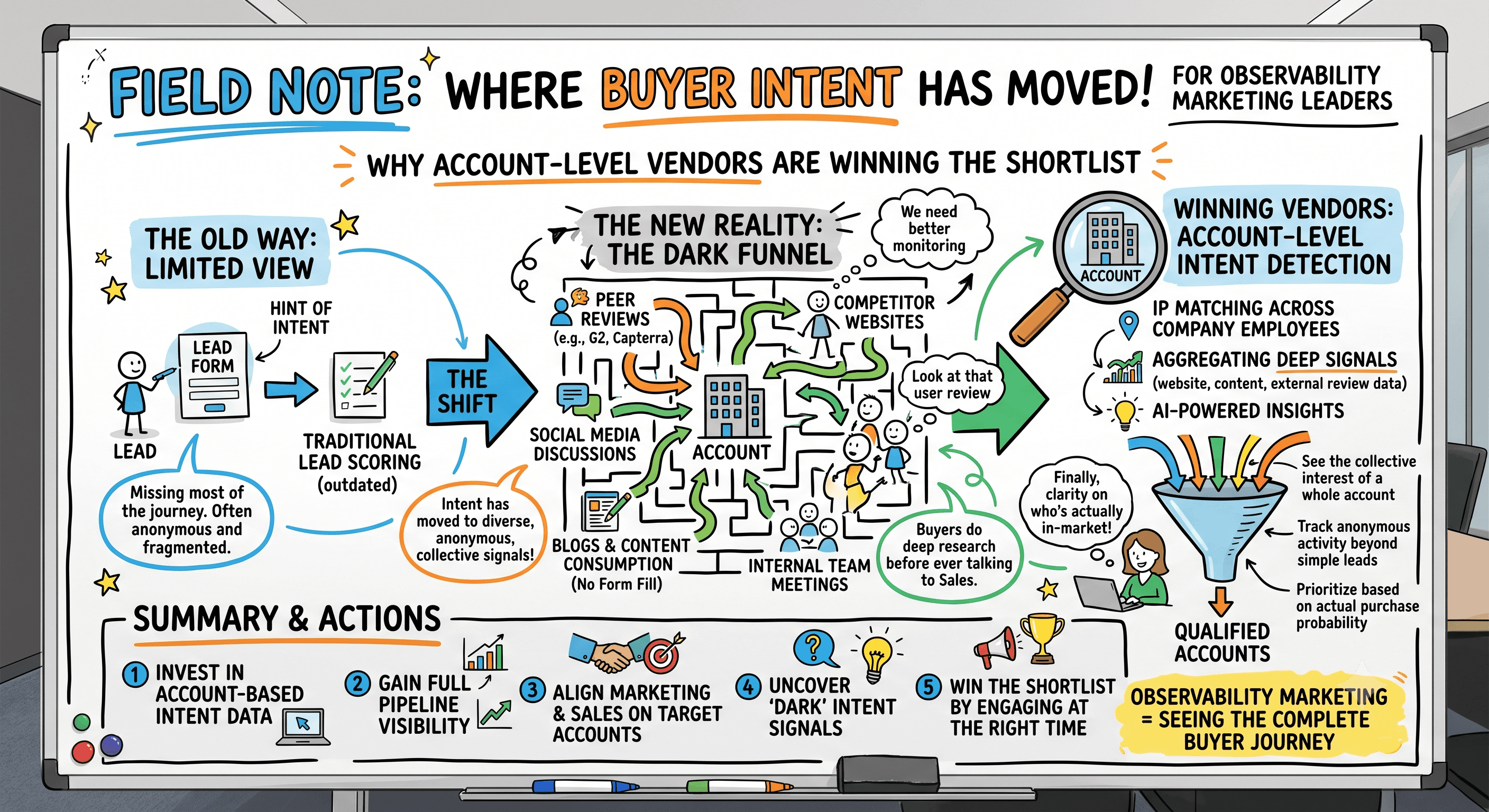

The category grew up. The messaging didn't.

For most of the last decade, an observability vendor could win attention with a capability claim. Metrics, logs, and traces. Full-stack visibility. Correlate everything. That framing built the category and, for a while, it separated the serious platforms from the also-rans.

In 2026 it separates nothing. Every vendor makes the same three claims, and the buyer has stopped listening to them. The harder question the market now asks — and the one most vendor messaging still fails to answer — is whether a platform can answer questions the team hasn't thought to ask yet, about systems they haven't built yet, at a cost trajectory finance will still tolerate after telemetry volume multiplies.

That is a different buyer, with different intent, moving through a different evaluation. For a marketing leader, the risk isn't that your product is behind. It's that your positioning is answering a question the buyer stopped asking eighteen months ago.

This piece maps the intents that actually drive observability purchases in 2026, and where a CMO should stand to meet them.

Intent one: "Prove it does something after ingestion"

The single most consequential shift is the commoditization of data collection. OpenTelemetry has become the default instrumentation layer, and its adoption in production keeps climbing while the experimentation cohort grows alongside it. The practical consequence is that instrumentation lock-in is fading as a differentiator. When the collector is vendor-neutral, "we ingest everything" is table stakes, not a selling point.

The value — and therefore the buyer's attention — has migrated downstream of ingestion. It now lives in what happens after the data lands: investigation acceleration, root-cause reasoning, outcome optimization, the quality of the insight rather than the completeness of the collection. Roughly 85% of organizations already use some form of generative AI in their observability practice, and that number is heading toward near-universal within two years. At that point, integrated AI stops being a feature and becomes an entry requirement.

But there's a trap in the AI story that most vendor messaging walks straight into. Buyers are explicit that they want automation with guardrails — policy-driven actions, approval workflows, and above all explainability that shows why the system flagged something and what data it used to decide. Black-box systems that can't show their work don't get trusted, and untrusted systems stay stuck in pilot. The revealing statistic: a large majority of teams are piloting AI, but only a tiny fraction have reached full production maturity.

How to position for it: Stop marketing the model and start marketing the reasoning surface. The winning message in 2026 is not "our AI is smarter." It is "our AI can defend its conclusion to your on-call engineer at 3am, and to your auditor at quarter-end." Lead with explainability, human-in-the-loop control, and the specific path from pilot to production. If your case studies can show a team that left pilot purgatory, that is your most valuable marketing asset — because it speaks directly to the fear underneath the buyer's intent.

Intent two: "Cost is now a strategy, not a line item"

Observability budgets are unusually resilient. The overwhelming majority of organizations are holding or increasing spend, and a meaningful share are planning specific increases. That is not a market under austerity. But — and this is the nuance vendors miss — budget resilience coexists with intense cost scrutiny. Nearly every team is taking active steps to reduce observability cost even as they protect the budget line.

The reason is structural. AI workloads generate an order of magnitude — sometimes two — more telemetry than traditional applications. A mid-sized team running a handful of AI features can watch monthly observability spend jump from the low tens of thousands into six figures. Telemetry storage can exceed the cost of the primary infrastructure it's meant to observe. So teams are consolidating toolsets, evaluating licensing and data-volume expenses, and in some cases simply switching off observability for less-critical environments to save money.

This creates a bifurcated intent that a CMO must hold in both hands at once. The buyer is not looking for the cheapest tool — "lower total cost" in their language means better value for money, measurable results that justify the price. But they are looking for pricing transparency and a defensible cost trajectory as volume scales.

How to position for it: Make your cost story a value story with a transparency spine. The message that lands is not "we're 90% cheaper" — that reads as commodity positioning and invites a race to the bottom. It's "here is exactly what you'll pay as your telemetry grows 10x, and here is the measurable outcome that spend buys." Sampling intelligence, pipeline filtering, adaptive telemetry, and consumption-based transparency are not just product features in 2026 — they are the vocabulary of trust with a finance-adjacent buyer. If your pricing model has a story about the AI-telemetry explosion specifically, tell it loudly, because that is the cost anxiety keeping your buyer awake.

Intent three: "Consolidation is a switching trigger, and I'm watching yours"

Vendor consolidation stopped being industry background noise and became a procurement input. When Palo Alto Networks acquired Chronosphere for $3.35B, and when platforms like ServiceNow's Lightstep marched toward end-of-life, buyers learned a lesson they now apply to every evaluation: the platform you pick today may not be commercially available, or strategically prioritized tomorrow.

The result is a market with unusually high switching willingness — around two-thirds of leaders say they'd change vendors within one to two years. The barriers that remain are operational (migration risk, integration complexity, training), not loyalty. And OpenTelemetry has lowered even those barriers, because instrumenting once against an open standard means switching is a matter of re-pointing an exporter rather than re-instrumenting an estate.

For a CMO this cuts two ways, and both are actionable. Every incumbent's consolidation event is a demand signal in your favor — a window where their customers are, briefly, in-market and anxious. And every rumor about your own stability is a silent objection you may never hear articulated.

How to position for it: Build a consolidation-response motion, not just a consolidation-response press release. When a competitor is acquired or sunset, the accounts on that platform enter a short, intense evaluation window — and the vendor who reaches them in that window, with a concrete migration path and a stability narrative, wins disproportionately. On your own side, treat platform stability and roadmap continuity as marketing messages, not just investor messages. In a market this switch-happy, "we'll still be here, and here's why" is a differentiator.

The intent beneath the intents: from category to account

Read those three shifts together and a deeper pattern emerges. The GenAI-explainability intent, the cost-trajectory intent, the consolidation-switching intent — none of them fire uniformly across a market. They fire account by account, on account-specific timing. One prospect is mid-way through a consolidation review this quarter because their incumbent just got acquired. Another just watched their AI-telemetry bill triple and has a CFO asking questions. A third is stuck in AI-pilot purgatory and is quietly evaluating whether explainability is the unlock.

These are not three market segments. They are three moments, and the same account moves between them over time. This is the real strategic shift for observability marketing in 2026: intent has migrated from the category to the account. The category-level trends report — the very genre this article belongs to — is now merely the price of entry. It demonstrates you understand the market. It does not tell your buyer that you understand them.

The vendors pulling ahead are the ones who can answer a much sharper question than "what are the 2026 trends?" They can answer: which of my target accounts is in a consolidation review right now, which just crossed a telemetry-cost threshold, and which is stuck in pilot — and what do I say to each, this week?

That is the difference between marketing to a market and marketing to a moment. The market rewards the second.

What this means for the marketing leader

If you run marketing for an observability platform, the 2026 mandate reshapes the funnel in four concrete ways.

Your top-of-funnel content has to graduate past capability claims. "Metrics, logs, and traces" and "full-stack visibility" are invisible now. The content that earns attention speaks to the moment — the explainability gap, the AI-telemetry cost curve, the consolidation window — because those are where the buyer's live intent sits.

Your mid-funnel has to carry proof of outcome, not proof of feature. The buyer's dominant anxiety is the insight gap: budget is available, but confidence that the tool produces actionable intelligence is not. Every case study that shows a team leaving pilot mode, defending an AI conclusion, or defending a cost line to finance is worth more than a feature comparison grid.

Your competitive motion has to be event-aware. Consolidation events are your highest-intent windows, and they are public. A marketing organization that treats each competitor acquisition or sunset as a triggered campaign — reaching the affected accounts inside the evaluation window — converts at a rate that untriggered outbound cannot approach.

And your positioning has to resolve the cost paradox honestly. Not cheapest. Not premium-for-its-own-sake. Transparent value with a defensible trajectory as telemetry explodes. The CMO who owns that narrative owns the finance-adjacent buyer who now sits at the evaluation table.

The observability buyer of 2026 is well-funded, deeply skeptical, standard-equipped, and switch-ready. They have heard every capability claim in the category. What they haven't heard — from most vendors — is a message that meets them at their specific moment. The platforms that learn to read and market to that moment, rather than to the category average, are the ones that will own the shortlist.

The trends are knowable. Everyone knows them. The edge is in the account.